Do you make a phone call to your bank to find out what your checking account balance is? Get on the right foot in your QuickBooks to make for increased accuracy from your first QuickBooks bank reconciliation onward.

When you create a new QuickBooks data file, there are two ways of establishing the opening balance in the checking account. The first method, which is a single entry, uses the bank balance found on the Balance Sheet, the tax return or the prior month’s bank reconciliation. This balance can be entered using a journal entry, or directly into the check register as either a single deposit or payment (depending on whether the balance is positive or negative).

To input the cash balance as one entry, however, does not allow you to separately clear individual bank transactions. A more effective approach is to enter the ending balance per the bank statement and the outstanding checks and deposits, each as a separate entry.

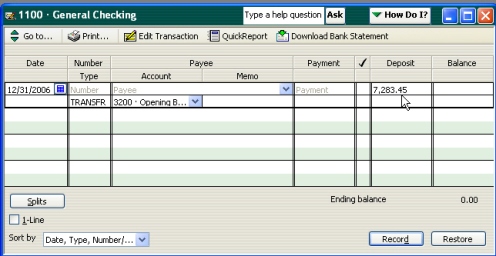

First, enter the bank statement balance directly into the check register using the start date and Opening Balance Equity as the offset account. (If a checking account is added after the start date, use the appropriate offset account or the transfer feature.) Then, input all outstanding checks and deposits, using the start date and the Opening Balance Equity account as the offset. The ending check register balance should still equal the final cash balance on your start date.

In the first reconciliation, a zero will appear in the Beginning Balance field. Enter the ending balance from the bank statement and click Continue. In the Reconcile window, select the amount representing the beginning balance per the bank statement, as well as the cleared transactions from the current statement. Click Reconcile Now when the difference equals zero. This method will allow you to individually select outstanding checks and deposits as part of the reconciliation process. If checks or deposits remain uncleared, they will appear in the next month’s reconciliation window.

Items to watch for when reconciling your bank account:

· Old outstanding checks and/or deposits: If a check or, more rarely, a deposit, needs to be voided within the current month, you may use the void check or delete deposit feature in QuickBooks. The issue becomes more complex if the check or deposit is from a “closed” prior period. If you simply void the check or delete the deposit, your bank balance will no longer match your financial statements because QuickBooks will recalculate the balance from the date of the voided/deleted transaction. To avoid this, record a deposit (for old outstanding checks) or write a check (for old outstanding deposits) on the account being reconciled, use the general ledger account from the original transaction. The date of the transaction, should be the date of the bank statement being reconciled.

· Grouping Deposits: When grouping deposits from undeposited funds, as in the case of credit card receipts or multiple checks, be very careful that the total of the deposit made to QuickBooks matches the actual deposit to the bank.

{ 3 comments }

Hi your blog posts are superb. Reconciliation of QuickBooks is no longer a mystery!

Thanks for explaining this process. Reconciling is so important to a businesses bookkeeping. Here at Intuit, we’ve just published a reconciling troubleshooting article: http://www.qblittlesquare.com/2011/05/reconciliation-trouble-clues-are-in-your-bank-statements/

Though it written for a Mac audience, the information is valid for any QuickBooks user. Thanks again for publishing this information.

Thanks Shelly! We are taking the liberty of commenting on and reposting your reconciliation tips! LB

Comments on this entry are closed.